Reviving Wind Energy Sector in India

As the world’s fourth largest wind energy market, India boasts an installed capacity of 53.6 GW, all of which is onshore, accounting for 20% of its non-fossil fuel generation. The wind sector’s growth trajectory has been remarkable, with installed capacity doubling between 2015 and 2025. Projections indicate that India could achieve 100 GW of installed wind capacity by 2030 , closely aligning with the National Electricity Plan’s target of 121 GW by 2031-32. Wind energy growth is central to India’s vision of ‘Viksit Bharat’, with policy and industry stakeholders recognising the critical need to accelerate repowering and site development. Challenges such as delays due to PTCC clearances and the need for streamlined micro-siting guidelines are being addressed to crash project timelines and improve efficiency.

WIND ENERGY

5/6/202618 min read

Executive Summary

India stands at a pivotal juncture in its wind energy journey, with the sector playing a crucial role in the nation’s renewable energy ambitions. As the world’s fourth largest wind energy market, India boasts an installed capacity of 53.6 GW, all of which is onshore, accounting for 20% of its non-fossil fuel generation. This capacity is heavily concentrated in Gujarat and Tamil Nadu, states that also present significant repowering opportunities due to the large number of ageing turbines.

The policy ecosystem in India has evolved substantially to support wind energy growth. Major initiatives include the National Offshore Wind Energy Policy (2015), guidelines for onshore development (2016), the National Wind-Solar Hybrid Policy (2018), and several recent measures such as competitive bidding processes, repowering and life extension policies, and viability gap funding schemes for offshore wind projects (2023-2024). The sector's regulatory landscape is further strengthened by revised lists of models and manufacturers, concessional custom duty certificates, and a clear bidding trajectory for renewable energy projects.

The wind sector’s growth trajectory has been remarkable, with installed capacity doubling between 2015 and 2025. Projections indicate that India could achieve 100 GW of installed wind capacity by 2030, closely aligning with the National Electricity Plan’s target of 121 GW by 2031-32. This progress is backed by an increasingly robust domestic manufacturing ecosystem, with 70-80% indigenisation and the presence of all major global players, either through joint ventures, subsidiaries, or Indian technology firms. The country’s component-wise manufacturing capacity is expanding, further enabling local content and minimising dependence on imports.

Wind energy growth is central to India’s vision of ‘Viksit Bharat’, with policy and industry stakeholders recognising the critical need to accelerate repowering and site development. Challenges such as delays due to PTCC clearances and the need for streamlined micro-siting guidelines are being addressed to crash project timelines and improve efficiency. Additionally, issues like reverse bidding for ISTS projects are under review to ensure fair and sustainable procurement practices.

In summary, India’s wind energy sector is a story of impressive progress, policy innovation, and manufacturing strength. However, realising its full potential requires continued momentum in repowering old projects, refining site development processes, and fostering a supportive policy environment. As India pursues its ambitious renewable energy goals, wind energy will remain a linchpin in the journey towards a sustainable and prosperous future.

India’s Wind Energy Story – A Mixed Bag

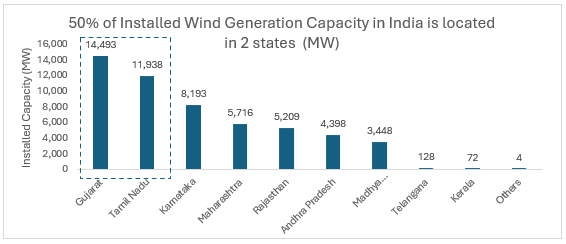

India has 4th largest wind energy installed capacity in the world at 53.6 GW, with all of the capacity onshore. As a share of the non-fossil fuel generation capacity of India, wind energy constitutes 20% of the share in India today. It is interesting to note that half of this capacity is concentrated in two states - Gujarat, Tamil Nadu – which also have the largest number of turbines that can potentially be repowered (figure 1).

Figure1: State of Wind Energy Capacity Installations Across India (Source: MNRE)

The growth of the sector has been impressive, with installed capacity doubling between 2015 and 2025. Given the current trends, it is expected that the installed capacity of wind will reach 100 GW by 2030,about 17% short of the planned target of 121 GW by 2031-32 as per the National Electricity Plan 2031-32. (GWEC 2025) (CEA, 2022).

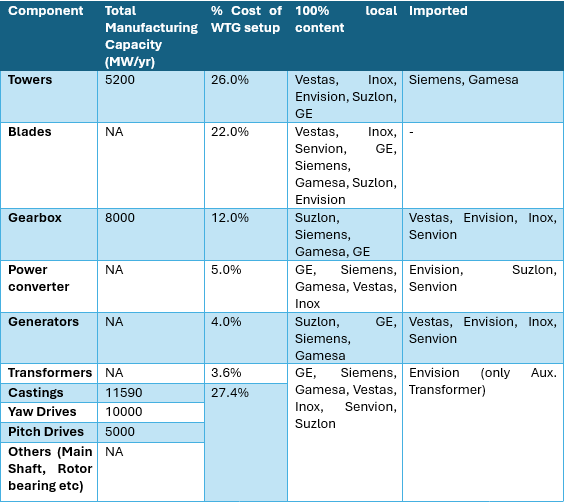

The growth of India’s wind energy sector has the necessary acceleration due to tail winds in the WTG (Wind Turbine Generators) components’ manufacturing ecosystem developed locally. India has emerged as a global manufacturing hub, with a strong supplier network and expanding capacities across all segments (table 1), with, around 70-80% indigenisation (MNRE, 2025). All the major global players in this field have their presence in the country with around 14 different companies, through (i) joint ventures under licensed production (ii) subsidiaries of foreign companies, and (iii) Indian companies with their own technology.

Table 1: Component Wise Capacity across Wind Ecosystem in India

Component

Total Manufacturing Capacity (MW/yr)

% Cost of WTG setup

100% local content

Imported

Current Policy Ecosystem in India

To encourage the wind sector, a variety of schemes have been rolled out by the government of India. A selection of important policy decisions, schemes and guidelines ranging from building offshore wind capacity to bidding guidelines and custom duty certifications, the main ones are briefly highlighted below:

National Offshore Wind Energy Policy 2015

The policy provides a framework for promoting large grid connected offshore wind energy in India. National Institute of Wind Energy (NIWE) identified as Nodal Agency for development of resources and facilitating clearances.

Guidelines for Development of Onshore Wind Power Projects 2016

MNRE came out with these comprehensive guidelines in 2016 for development of wind power projects in the country in a cost effective and efficient manner. The policy touches upon various aspects such as site selection and micrositing, grid connectivity, quality assurance and decommissioning.

National Wind-Solar Hybrid Policy 2018

The policy provides a framework for promoting grid connected large wind-solar PV hybrid system for optimal and efficient utilization of transmission infrastructure and land. It reduces the variability in renewable power generation and achieving better grid stability. This policy was borne by the recognition of overlaps in large areas with both wind and solar resources having high to moderate potential.

Guidelines for Tariff Based Competitive Bidding Process for Procurement Power from Grid Connected Wind Power Projects - 2023

The policy has been delineated to facilitate renewable capacity addition and fulfilment of Renewable Purchase Obligation (RPO) requirements of distribution licensees. It also enables long term sale and purchase of power at inter-state and/or intra-state levels to derisk the sector as a whole. Under the policy, open competitive bidding is conducted, with appropriate risk-sharing between various stakeholders put in place to enable competitive prices is undertaken, improve bankability of projects and ensure reasonable returns to the investors.

National Repowering & Life Extension Policy for Wind Power Projects – 2023

The policy acknowledges the need for repowering/refurbishing old wind energy projects and outlines the framework to implement repowering through respective State Nodal Agency in the State or the appointed Central Nodal Agency. Arrangements are provided under the policy for power procurement by state, with surplus to be procured through bids by central agency.

Bidding Trajectory for Renewable Energy Power Projects - 2023

To encourage development of wind projects in India, a bidding trajectory has been outlined by MNRE. As per the trajectory, bids for at least 10 GW per annum of Wind Energy capacity are to be issued each year from Financial Year (FY) 2023-24 to FY 2027-28. Additionally, year-wise targeted bid capacity are to be allocated among Renewable Energy Implementing Agencies (REIAs).

Viability Gap Fund (VGF) Scheme for Offshore Wind Energy Projects - 2024

To encourage development of offshore wind in India, a Viability Gap Fund with a total outlay of ₹7,453 crore has been set up. MNRE had issued Guidelines for implementation of the VGF scheme in September 2024.

Revised List of Models & Manufacturers (RLMM)

RLMM list has been issued by MNRE to facilitate State Nodal Agencies (SNAs), investors, lenders and developers. This list is to ensure that type and quality certification by an Internationally Accredited Certification Body shall be a mandatory requirement for manufacturers of wind turbines and their components, and both certifications should mandatorily include Hub and Nacelle assembly/manufacturing facility in India.

Concessional Custom Duty Certificates (CCDCs) 2023-2025

To facilitate the import of critical components required for manufacturing of WTG in India, Concessional Custom Duty Certificate scheme was launched by the Ministry of Finance. Under this, the government provides financial incentive in the form of Concessional Custom Duty on the identified components, and details a procedure to avail this benefit.

Wind Energy Growth is Critical to Achieve Viksit Bharat Ambitions

The role of wind energy in Viksit Bharat is a rather important one. Currently, the capital cost for wind energy is ₹7-8 crore/MW, which is 50% higher than the utility scale solar power plant (₹4.5 crore/MW); this is often used to raise questions on the role of wind energy for growing India’s non-fossil fuel capacity in 2047. However, wind energy offers several important advantages that often gets overlooked (GWEC, 2025):

• Optimizing generation cost: wind energy is essential for achieving the lowest-cost energy mix, primarily arising from higher capacity utilization compared to solar energy. The likely solar and wind Capacity Utilization Factors (CUFs) have been reported to be 22.97% and 40.8% respectively.

• Effective Round the Clock (RTC) Energy: Despite higher capex, a higher share of wind energy in the RE generation mix results in lower per unit costs, making RTC energy more cost-effective. Increasing wind’s share in RTC energy, with minimal solar additions, enhances resource utilization and energy supply efficiency. This is due to the fact that wind energy serves as the cheapest power source in the evening & early morning hours, while there is lower generation & higher cost during the daytime, which are the key solar hours.

• Optimizing transmission network utilization: Increased wind capacity can ensure better utilization of transmission lines, reducing overall transmission network requirement, with estimates noting capital expenditure savings between 35-40% with increase in wind capacity.

• Optimizing Storage Requirement: A higher amount of wind is expected to ease the pressure on the storage requirements for the system which will be required with solar to manage the transition

Wind has been seen as a critical contributor to India’s net zero ambitions, especially when aligned with the desire to achieve the Viksit Bharat by 2047 goal. As per NITI Aayog’s Net Zero Scenario assessment, the ambitious Viksit Bharat scenario would translate to wind generation capacity reaching 680 GW by the year 2050, or more than 11 times the current installed capacity. To achieve this target, the annual capacity addition of at least 25 GW has to happen annually. In contrast, the addition rate of 5.5 GW was expected for 2025 – this is a fifth of the desired strike rate.

To fully realize the potential of wind energy in India, the wind energy sector’s challenges need to be tackled head on. An assessment across the landscape has revealed specific problems that have stymied the growth of wind energy in India. These include a range of issues from site availability, reverse bidding, clearance related challenges to the lack of clarity on ambitions on offshore wind.

Large portions of Rajasthan, Gujarat, Madhya Pradesh, Maharashtra, Karnataka, Andhra Pradesh, and other western, central, and southern states have excellent wind resources; however, many of these areas also have great solar potential, creating competition around the availability of land. A push for hybrid wind-solar solutions at the policy front, we have seen significant movement –70 GW of hybrid/RTC/Firm and Dispatchable Renewable Energy (FDRE) Projects were under various stages of implementation across India as of 31 December 2025; however, it is evident that they were partial towards the integration of various kinds of hydro power projects, including pumped hydro energy storage (PHES) projects. Further, there are concerns regarding the existing land usage patterns – in many of these places, land is used for agriculture, inhabited, or has ecological value; converting such land for wind farms may face resistance, making access to good sites difficult. These factors are cumulatively leading to a shortage of quality wind sites across India.

Repowering tackles the land-scarcity issue at its root by extracting far more energy from the same land parcels already occupied by old wind farms. This can help to avoid fresh social conflict, bypasses land-title complications and makes optimal use of scarce high-wind locations otherwise saturated. Similarly, offshore wind fundamentally shifts deployment away from agriculture, forests, habitations, and fragmented ownership regimes by enabling large-scale capacity addition without competing for land. For coastal industrial clusters, ports, and green hydrogen hubs, offshore wind also reduces transmission distances and congestion, further easing pressure on inland land and evacuation corridors.

Additionally, to enable these transitions, issues related to clearances associated with turbine micro-siting and connectivity clearances such as the one from Power & Telecommunication Coordination Committee (PTCC) clearances need to be accelerated. Not addressing these challenges can significantly delay projects, thereby stalling efforts to sharply increase India’s wind power installations.

Repowering of Old Wind Projects in India Needs to be Given Momentum

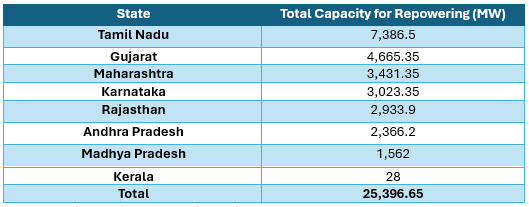

25 GW of wind energy capacity located across some of India’s best wind energy potential sites have been identified by MNRE to have the potential of repowering. Going by the clause in the National Repowering Policy of achieving an increase in generation capacity by at least 1.5 times, the sites can be refreshed to host 37.5 GW wind power capacity. This is because new windmills can operate at hub heights over 150 metres and generate more electricity per unit of machine capex using turbines of over 3 MW capacity. This can leverage high-generation-potential sites that now have the older generation turbines. For instance, a new 3 MW windmill with a plant load factor (PLF) of 34-36% can potentially generate 200% more electricity versus a 1 MW old machine at the same site with a PLF of 22-24% (CRISIL, 2023).

Almost 47.5% of this repowering potential is concentrated in Tamil Nadu and Gujarat alone (table 2).

Table 2: Repowering Potential Across Wind Energy States of India

Source: National Wind Repowering Policy

State

Total Capacity for Repowering (

In view of the given situation, in 2023 MNRE launched the National Repowering and Life Extension Policy, 2023. The policy proposed to set up a repowering agency to aggregate projects. These agencies are mandated to identify potential turbines for repowering and can nominate any State/Central PSEs as Wind Repowering Project Aggregators (WRPA) to initiate the project or elicit interest from private developers. The policy also stated that there will be no obligation for discom/procurer to buy the additional power generated at a fixed rate. Consequently, six states – Tamil Nadu, Gujarat, Maharashtra, Rajasthan, Andhra Pradesh and Karnataka - have taken one of the three approaches:

1. Come out with their individual state level policies

2. Integrate clauses on wind repowering into their Integrated Clean Energy Policies

3. Adopt the central policy to the state level through executive order of the electricity regulatory commission

Despite progress on the policy front, the blades of the wind repowering are moving slow with negligible improvements. the biggest challenge is the cost of repowering – as it tends to be more than the cost of developing a greenfield project due to the additional costs such as impacts of decommissioning of an old assets, foregone revenue for the remaining life of the existing projects, revenue loss during the construction period, salvage value of the old assets etc (Idam, 2018). This also eventually impacts the landed cost of power – a CRISIL assessment had stated that a tariff of ₹4/kWh is needed for incremental capacity (CRISIL, 2023), higher than ₹3.6 – 3.9 /kWh discovered in SECI auctions, impacting the willingness to procure or commission.

In India, there are multiple owners of wind turbines in the same wind farm. A large number of these projects came up in an effort to avail the high Accelerated Depreciation benefit (80% till 2012) that the wind turbine owners received, where ownership would often be of the nature of just 1- 2 turbines per owner. Repowering of these old turbines will reduce the actual number of turbines, complicating the ownership issues of new turbines, and clearances would be needed from multiple owners to even initiate the project (Idam, 2018).

Absence of assured long-term power offtake arrangements, especially for additional power impacts bankability, remains unaddressed. Both at the central and state levels, repowered project developers have been directed to adopt one of the three approaches:

1. Self-consume power in captive arrangement

2. Sell to power exchange

3. Seek bilateral agreement in open access

Discoms are neither mandated to procure additional energy nor conduct any procurement rounds through bidding for the same. This causes significant uncertainty for developers, since lack of sale of additional generation will directly threaten project financials.

Another major issue is the inadequate grid evacuation and transmission infrastructure at legacy sites limiting redevelopment. A large number of old projects tend to be connected to evacuation infrastructure that cannot cope with additional generation. E.g. in Tamil Nadu, most of the windfarms that house projects with completed life of more than 15 years are connected to the 11 kV lines for the evacuation of power. However, post repowering, the capacity and aggregate generation may increase by two and three times respectively. There is a need to upgrade the existing infrastructure such that all the energy generated can be evacuated properly without any congestion for evacuation of wind power and without any forced generation curtailment.

A close look at the challenges reveals that a large portion of them can be tackled suitably if there is one particular agency that can perform the necessary aggregation to achieve scale. Within the policy, clause 7 (ii) clearly states that:

“State Nodal Agency (SNA)s /Central Nodal Agency (CNA) may identify the potential turbines for repowering. In such cases SNAs/CNA either nominate any State/Central Public Sector Enterprise (PSEs) as Wind Repowering Project Aggregators (WRPA) to repower the project or elicit interest from private developers for the same. The selection of the private developer as WRPA shall be through a transparent mechanism based on minimum technical & financial criteria. The indicative parameters for selection of WRPA may include Quality Assurance Certificate, Financial turnover, Experience, Repowering plan, Old asset evaluation, Consent agreement from the existing owners, Indication of land rights arrangement, Asset disposal plan etc.”

Given the fact that standalone projects will be few and far between, the need for an aggregation agency becomes all the more significant. Therefore, it is suggested that Amendment to National Repowering and Life Extension Policy, 2023 be made to set up a National Implementing Agency (NIA). This NIA can be empowered to undertake the following functions to create the conducive environment for redevelopment to achieve the policy objectives:

· Develop Statewide Repowering Action Plans with timelines and ownership mapping

· Aggregate fragmented assets, structure new projects, enable new tariff discovery

· Ensure offtake through NIA, launch state-level hybrid tenders (Wind + Solar + BESS) with bidding trajectory

Reverse Bidding by SECI for ISTS Projects Needs to be Re-Examined

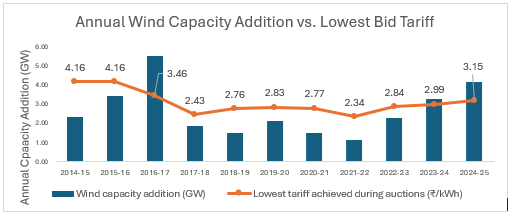

Reverse bidding, while beneficial for the growth of the overall renewable energy sector, has proven to be detrimental to the wind power’s growth. The introduction of reverse bidding has led to significant slowdown in capacity addition - between March 2017 and March 2023, India added just 10.3 GW, or just 1.7GW/year. The tariffs discovered during the reverse bids proved to be unsustainable, as the tariffs were not reflective of the development costs. Tariffs during the first phase of reverse bidding-based auctions came down from ₹3.46/kWh to ₹2.44/kWh, eventually settling at around ₹2.80/kWh. When reverse auction was given up for ‘closed bidding’ system (here, bids are opened and the lowest bidder is declared the winner), tariffs rose. This was the case seen in the SECI’s sixteenth tranche for setting up of 1350 MW Inter State Transmission System (ISTS)-connected Wind Power Projects, where winning tariffs were between ₹3.60/kWh and ₹4.24/kWh. Latest reverse auctions have also since led to similar tariffs e.g. SECI Tranche XVIII saw the discovery of a tariff of ₹3.98/kWh.

Figure 2: Capacity addition slowed down substantially after reverse bidding was introduced in the year 2016-17. Removal of reverse bids in 2023-24 led to a rise in annual capacity addition (note: 2014-15 and 2015-16 tariffs are essentially lowest feed-in tariffs in states. The transition from feed in tariffs to reverse bidding took place in 2016-17. Also, there is an 18-month timeline from bidding to commissioning of projects, which gets reflected in numbers accordingly)

However, the problems with reverse bidding are not restricted to just the price discovery. Reverse bidding has also led to unfair concentration of wind projects in a few states (IEEFA, 2024). Because of reverse bidding, developers focus on only those states that have the highest wind potential (Gujarat and Tamil Nadu) to meet low, competitive tariffs – despite land and infrastructure availability, investors do not prefer states like MP, Rajasthan and Maharashtra.

An analysis of the MNRE’s 2023 Guidelines for Tariff Based Competitive Bidding Process for Procurement Power from Grid Connected Wind Power Projects highlights the fact that Clause 6.2.3 of the guidelines allows procurers to undertake reverse bidding, which has been utilized by SECI. The clause specifically reads:

“The procurer may also opt for reverse auction for final selection of bidders, in such a case, this will be specifically mentioned in the notice inviting bids and bid document. The procurer may disclose in the Request for Selection (RfS), the prevailing incentives available to the Wind Power Generations (WPGs).”

It is therefore recommended that an amendment to the guidelines should be undertaken by MNRE to remove Clause 6.2.3. With only closed bidding in the fray, confidence will be generated in the developer community and projects can be spread out evenly.

Site Development Issues Need to be Sorted

While more operational in nature, site development related issues have had a major impact on the development of the wind energy projects in India. The impact on onshore side greenfield projects and repowering of old projects need to tackle them suitably. Two major issues – clearances from the Power and Telecommunication Coordination Committee and the micrositing related issues need focused attention.

PTCC Clearances Causing Delays, Need a Revisit to Crash Timelines

The history of the Power and Telecommunication Coordination Committee (PTCC) underlines its importance and relevance to this day in many aspects. PTCC was born out of the All India Power Engineers Conference held in February 1949 that recognized the need for a Central Standing Committee for co-ordination of Power and Telecommunication Systems and had recommended the same to the Central government of the time. Based on the recommendations of this conference, a Committee was formulated in May 1949, headed by the Central Electricity Authority (CEA), to resolve technical issues, evolve standards and ensure safe co-existence among various Power and Telecom operators with focus on overhead cabling to avoid electromagnetic interference between power lines and telecommunication lines when both were laid in close proximity . State level sub-committees were set up in 1967 to tackle the issues of installing 33kV – 132 kV feeder lines to ensure smooth execution.

Although CEA has simplified the process and procedures over the years, a few challenges continue to impact project execution. Clearance required for an underground 33kV feeders are often delayed due to infrequent meetings of the committee to resolve this challenge. The National Solar Energy Federation of India (NSEFI) has noted that, according to the PTCC’s own website, the permission granting process could take at least 32 weeks. However, a few key factors need to be considered:

A. The technology of telecommunications has changed drastically with the mass penetration of optical fibre cables (OFC) as well as wireless lines. The use of OFC in the telecom network and polythene insulated jelly filled cable have considerably reduced the electromagnetic interference between power and telecom lines.

B. All solar projects are built in rural areas, where landline connections are miniscule. Of the 1.1 billion telephone connections in India, rural landline subscribers comprise just 3.91 million.

C. Further, 33kV feeder lines for wind turbines are now laid underground, which further reduces the chance of electromagnetic interferences.

Considering the technological change, it is recommended that the Ministry of Power and the Central Electricity Authority (CEA) amend the PTCC Approval Process for swifter clearances The “Rules of Business of the Central Standing Committee for Co-ordination of Power and Telecommunication Lines” under Resolution No.EL.II-151 (7) dated 30 th May 1949, Amended by EL.II-141 (7) dated 29 th August 1949 there is a need to ensure smaller timelines; this may be through deemed approvals or through third party mandates.

Micro Siting Guidelines Need to be Streamlined

Micro-siting refers to the precise placement and arrangement of wind turbines within a selected project site, following initial site selection. This is important, the selection of optimal locations within a wind farm for individual turbines can help to maximize the energy capture and minimize the interface between the turbines.

As part of the “Guidelines for Development of Onshore Wind Power Projects”, micro-siting guidelines have been laid out specifically. Further to the OM No. 8(12)/2012/D(Coord) dated 15.10.2013 of the Ministry of Defence, there is also the involvement of the Ministry of Defence for micro-siting clearances, primarily due to concerns about aviation and radar interference. Minor adjustments to turbine coordinates necessitate developers to seek fresh approvals including No Objection Certificates (NOCs). However, international practice often allows planning “micro-siting tolerances” around consented turbine coordinates (about 50m more or less in Scotland and Ireland for instance) on the basis that such changes do not materially alter environmental or visual impacts. Similarly, in Australia, approvals specify a “development envelope” (a box or polygon) within which turbines may be micro-sited, provided it does not materially increase environmental impacts. Therefore, it is recommended that MNRE and Ministry of Defence amend the suitable guidelines on micrositing, to provide for a development envelope with the necessary qualifications, to reduce the need for revisiting approval processes on the exact location of the turbine.

Conclusion

In summary, while the PTCC and its approval framework have played a vital role in ensuring safer and better coordination between power and telecommunication infrastructure, evolving technologies and practices require reforms in the legacy processes. The widespread adoption of optical fibre and underground cabling, coupled with the rural setting of most wind energy projects, has significantly reduced electromagnetic interference risks. Streamlining approval timelines and introducing concepts like deemed approvals or third-party mandates, as well as adopting international best practices in micro-siting tolerances, will support India’s ambitions for rapid renewable energy expansion. Proactive amendments by the Ministry of Power, CEA, MNRE, and Ministry of Defence will help facilitate ease of doing business, encourage investment, and accelerate the country’s transition to a clean energy future.

Sources:

https://cea.nic.in/wp-content/uploads/irp/2023/06/NEP_2022_32_FINAL_GAZETTE.pdf

https://mnre.gov.in/en/wind-manufacturing/

NITI Aayog. (2026). Scenarios Towards Viksit Bharat and Net Zero - Sectoral Insights: Power (Vol. 7) https://niti.gov.in/sites/default/files/2026-02/Scenarios-Towards-Viksit-Bharat-and-Net-Zero-Sectoral-Insights-Power.pdf

Anna-Katharina von Krauland, Mark Z. Jacobson, India onshore wind energy atlas accounting for altitude and land use restrictions and co-located solar, Cell Reports Sustainability, Volume 1, Issue 5, 2024, 100083, ISSN 2949-7906, https://doi.org/10.1016/j.crsus.2024.100083.

Halder, P. (2024, June 26). Ground realities: Making land work for renewable energy. India Development Review https://idronline.org/article/climate-emergency/ground-realities-making-land-work-for-renewable-energy/

https://www.giz.de/en/downloads/11_Repowering_Study_Idam.pdf

https://seci.co.in/uploads/tenders/bidders/bidder_6850f5431e54c0_39758349.pdf

https://www.financialexpress.com/opinion/reviving-the-wind-sector-challenges-suggestions/2454196/

Mani Jabez, R., Victor, K. Wind resource assessment and optimization of wind farm layout at Kayathar, Tamil Nadu, India using WAsP. Discov Appl Sci 7, 517 (2025). https://doi.org/10.1007/s42452-025-07083-1

https://tethys.pnnl.gov/sites/default/files/publications/SNH-2017-Siting-Designing-Wind.pdf

https://www.planning.nsw.gov.au/sites/default/files/2023-03/wind-energy-guideline.pdf

Contact:

For digital copies of the report, contact:

Month of Publication:

May, 2026

Disclaimer:

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without permission in writing from Bodhaka Advisors LLP.

All images used for cover design are sourced through creative commons licensing.

Contact

Reach out for tailored climate-specific business advice

info@bodhaka-advisors.com

© 2026. All rights reserved.